Adam Eagleston, CFA

CIO

Will Brown

CEO/Managing Partner

April 2026 Update: Player Piano

Part I – Summary

April 2026 Update: Player Piano

Key Takeaways:

- Those who live by electronics, die by electronics.

- Unbridled AI enthusiasm began to wane in late January, with massive spending from most of the Mag 7 starting to concern investors and kindling fears of obsolescence for some companies.

- Investors then faced an unforeseen geopolitical event that spiked oil prices, increased inflation concerns, and decreased odds of a Fed rate cut.

- Despite the tumult, at the index level stocks suffered only modest declines, though that masked considerable damage beneath the surface.

- And a step backward, after making a wrong turn, is a step in the right direction.

- Investors are trying to figure out what is the right direction after a volatile Q1.

- Geopolitical events are proving to be headwinds for GDP growth, inflation, and Fed policy.

- Whether earnings can accelerate despite these headwinds is key as to whether the current lower valuations (relatively speaking) for equities represent a good opportunity for investors.

- I want to stand as close to the edge as I can without going over.

- We seemingly stepped back from the edge of a massive escalation with Iran, with a tenuous ceasefire now in place.

- However, the delayed effects of the disruption in the flow of oil (and associated products) may not be fully reflected just yet.

- As experienced advisors, we have perspective that the machines may not.

SUMMARY: before you close the email, please know these three things.

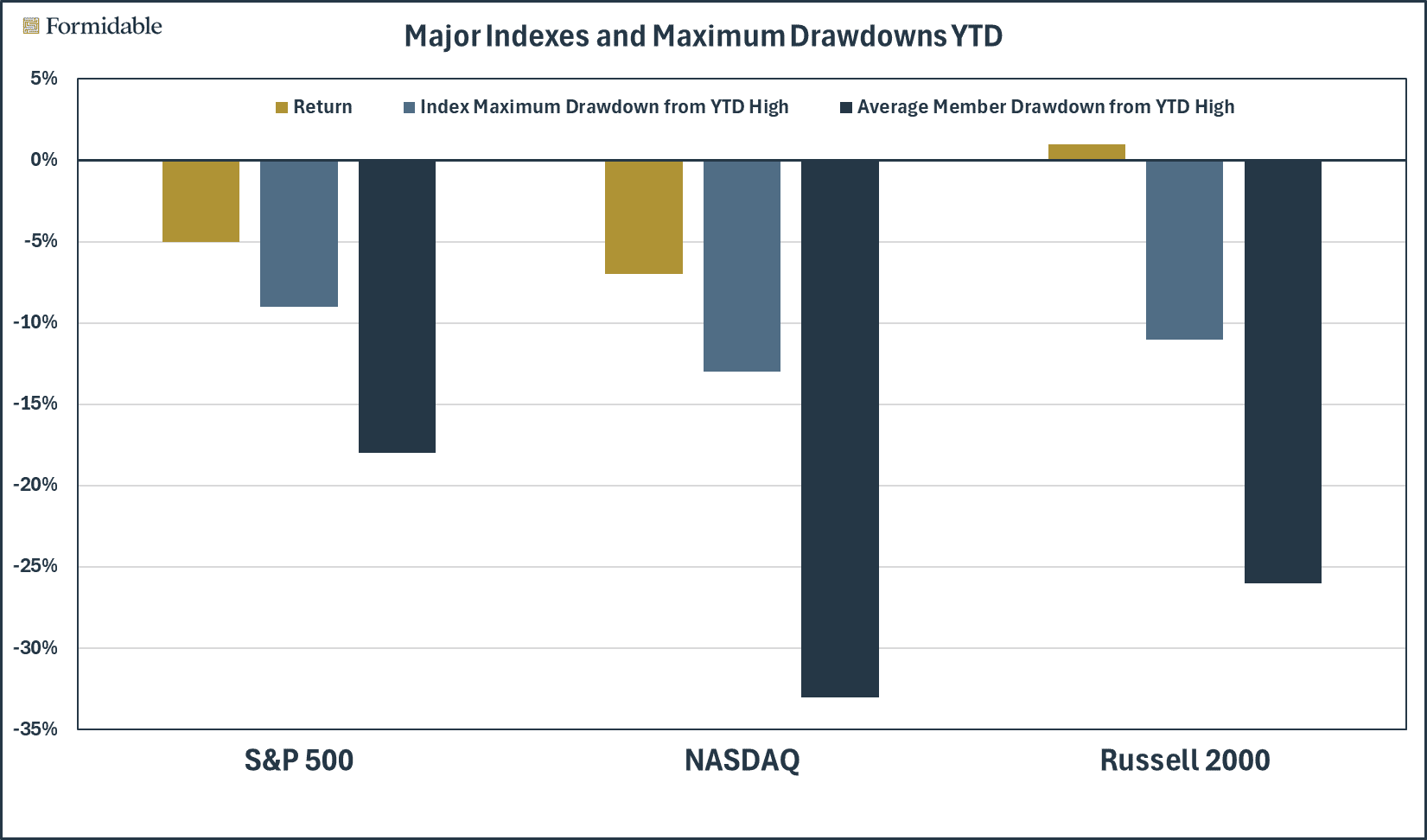

- The average stock within a given index has experienced a drawdown much larger than the index (see graph below).

- Earnings expectations have generally increased for 2026, bring multiples for the S&P 500 index into the “only slightly expensive” category.

- The geopolitical environment remains dynamic and requires a disciplined approach to managing portfolios.

Source: Bloomberg, Schwab

Part II: Q1 Recap – “Those who live by electronics, die by electronics!”

2026 began similarly to how 2025 ended, with euphoria around stocks and the prospect of continued economic growth driven by the AI boom leading to a fourth consecutive year of double-digit gains. As of late January, as the S&P 500 hit an all-time high, it looked like that story was playing out.

However, as Kurt Vonnegut wrote in his prescient 1950s novel Player Piano, “Those who live by electronics, die by electronics.” From a market perspective, as we will see shortly, that has proven to be the case. Below is an excerpt from what Claude cranked out when we tasked it with analyzing the quarter using Player Piano as the theme; more on that later, too.

At the index level, stocks were mixed. Large caps, especially U.S. technology stocks, struggled in Q1. Small caps and non-U.S. stocks were positive, albeit modestly, and mostly due to a deus ex machina rally on March 31, the result of a ceasefire announcement with Iran (versus the possibility of a civilizational erasure that had been threatened on Twitter). Commodities were the big winner, owing to the aforementioned conflagration. Also dampening market enthusiasm were concerns over AI spending, as well as the potential obsolescence of any number of companies due to the threat posed by AI, with a sprinkling of private credit fears thrown in for good measure. So much has happened that the operation to seize Maduro in Venezuela and the Supreme Court ruling on the Trump tariffs barely register.

| Fund/Index | 1-Month | 3-Month | 1-Year |

| S&P 500 INDEX | -5.09 | -4.63 | 16.33 |

| Invesco S&P 500 Equal Weight E | -5.97 | 0.61 | 12.59 |

| Russell 2000 Index | -5.17 | 0.58 | 24.08 |

| NASDAQ Composite Index | -2.76 | -12.32 | 13.33 |

| MSCI EAFE Index | -7.83 | 1.15 | 22.82 |

| MSCI Emerging Markets Index | -9.25 | 3.80 | 32.73 |

| Bloomberg US Treasury Total Re | -1.79 | 0.03 | 4.30 |

| Bloomberg US Agg Total Return | -4.22 | 0.19 | -0.49 |

| Invesco DB Commodity Index Tra | 15.34 | 29.47 | 31.97 |

Source: FactSet (as of most recent month end)

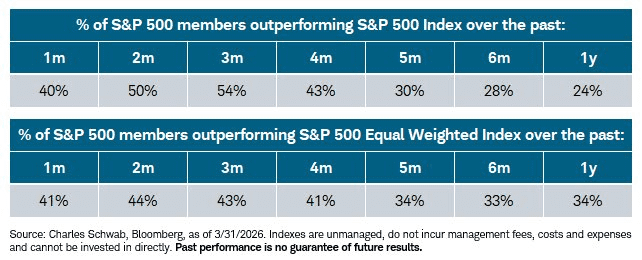

While the last three months have seen a modicum of broadening (i.e., more stocks are outperforming), the odds have been stacked against stock pickers for the last 12 months in a big way.

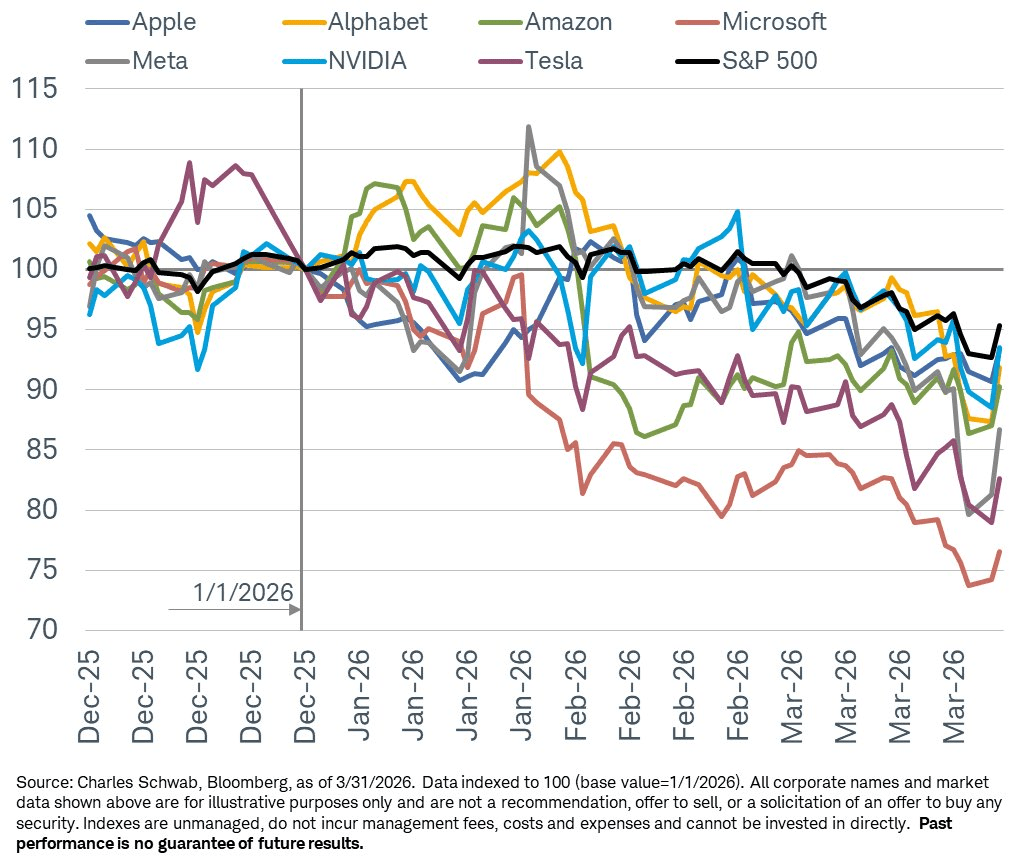

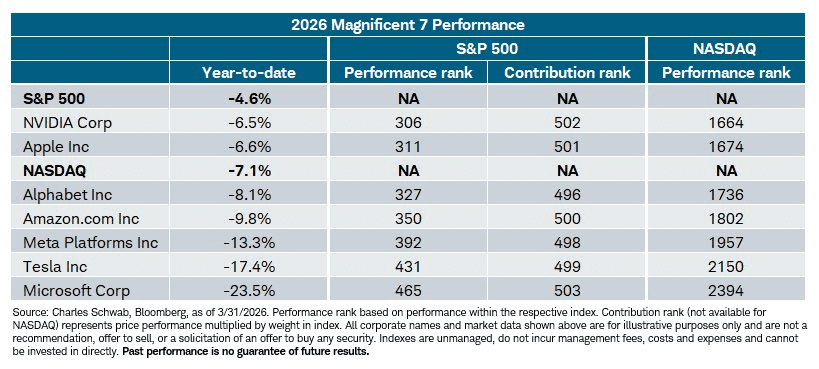

A major reason we have seen broadening is the cracks that have started appearing in the façade of the Magnificent Seven stocks. All of them lagged the index in Q1; Microsoft was down over 25% at one point as software stocks were particularly impacted by concerns over obsolescence from AI tools. Rampant capex harmed the others, while Nvidia and Apple were only marginal laggards; the former as it benefits from AI spending and the latter because it has (so far) taken a disciplined approach to AI capex.

Q2 and 2026 Outlook – “And a step backward, after making a wrong turn, is a step in the right direction.”

Markets took a step backward during Q1. In some cases, as mentioned, it was a result of concerns over spending on AI. Only time will tell if this massive outlay of capital is a step in the right direction, both for shareholders as well as the economy. In point of fact, those two things could easily diverge. As Vonnegut states, “That would be the third revolution, I guess—machines that devaluate human thinking.”

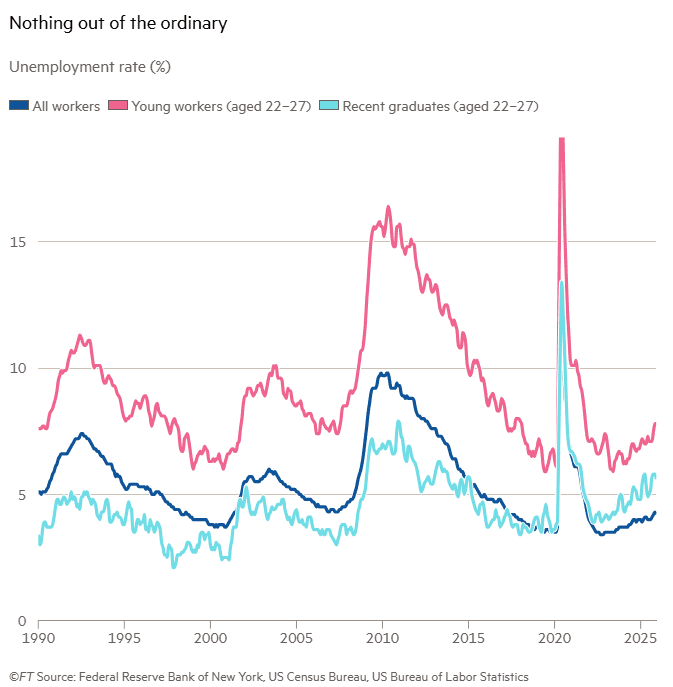

We are starting to see hints of this displacement of knowledge workers, though it is more anecdotal than supported by data (so far). Per the FT, “The unemployment rate for recent grads has ticked up since 2023 or so. But we’re not seeing a divergence in the trend in the unemployment rate between the fresh college graduates and non-graduate workers of the same age, as you would expect if AI were the cause.”

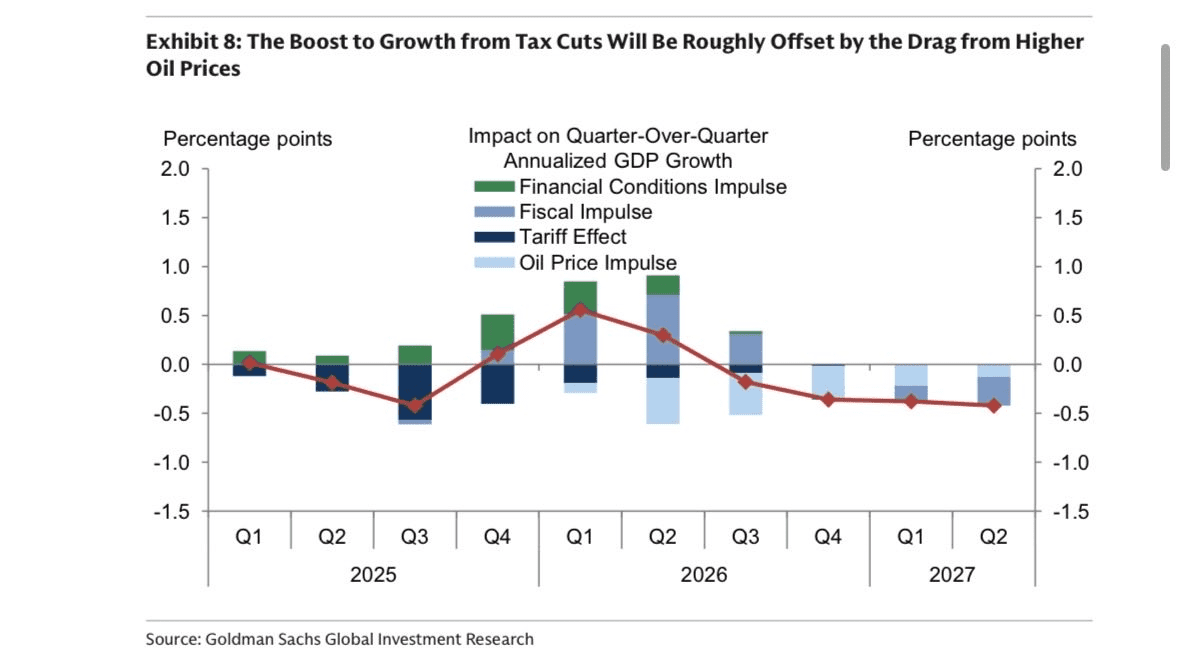

On the political (and geopolitical) front, the good news in terms of incremental stimulus from the OBBA looks to be meaningfully offset by higher energy prices.

In terms of the factors we track, three deteriorated (Inflation, GDP growth, and Fed Policy) while multiples and earnings growth actually improved. In general, the bias is slightly tilted toward the negative side. For more details on all of our factors, click here.

| More Negative | Neutral | More Positive | |||

| Inflation | ← | ||||

| GDP Growth | ← | ||||

| Fed Policy | ← | ||||

| Interest Rates | ≈ | ||||

| Credit Spreads | ≈ | ||||

| Stock Multiples | → | ||||

| Earnings Growth | → | ||||

| Deteriorating | ← | ||||

| Stable | ≈ | ||||

| Improving | → | ||||

Conclusion – “I want to stand as close to the edge as I can without going over.”

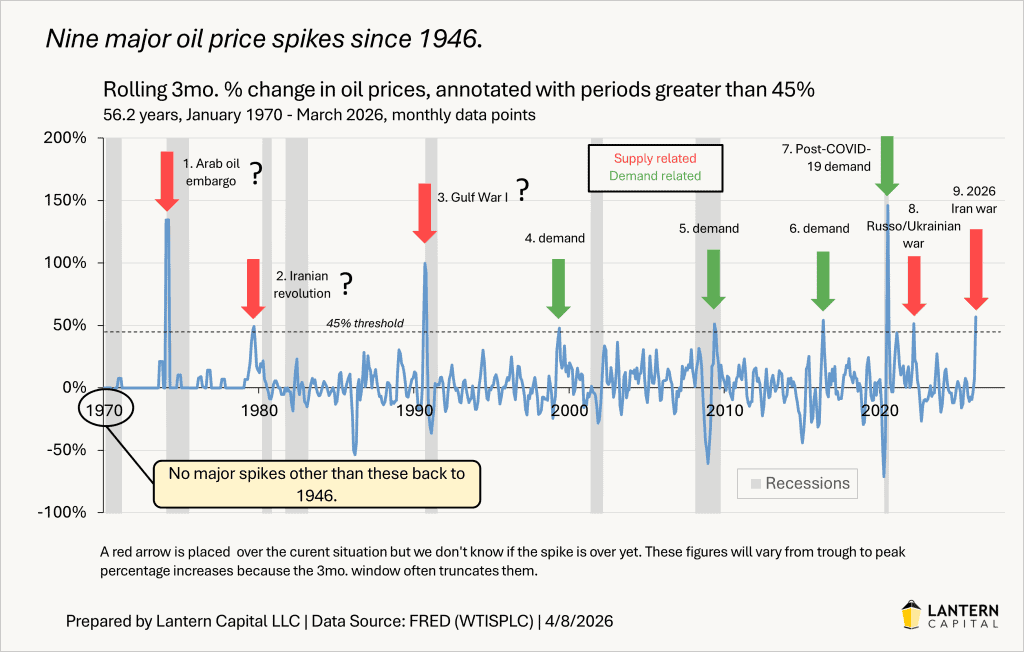

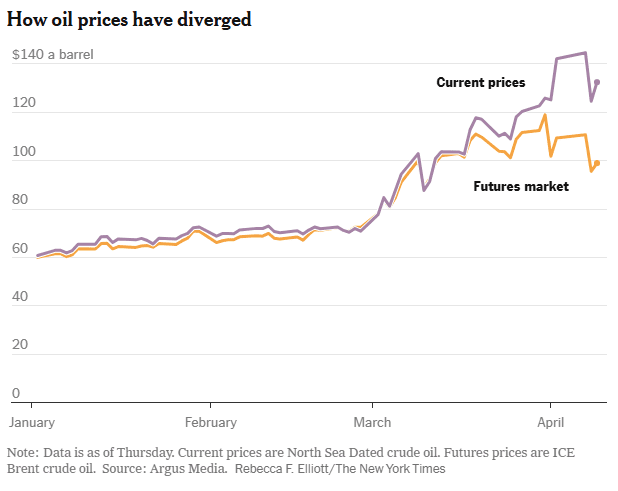

There have been times over the past few weeks where it has felt like we were at the edge. The rhetoric and images from the conflict in the Middle East certainly evoked that sensation. While we are optimistic that the tenuous ceasefire in place holds, in some ways the damage, economically speaking, has already been done. Nine (9) million barrels of oil per day are not moving. This is not a problem that abates immediately when (if?) the conflict is permanently resolved. It takes time, not to mention expensive, critical energy infrastructure that has been severely damaged or destroyed across the Persian Gulf. Related critical petroleum byproducts (sulfur, fertilizer, helium, etc.) are also in short supply and time is not our friend (European airports will run out of fuel in three weeks if something does not get oil flowing soon).

In short, supply-related oil price spikes are often associated with adverse economic consequences, though 2022 was a notable exception. Also, importantly, the prices below are for oil futures contracts; right now, oil for physical delivery (the kind a refinery needs) is trading at much higher prices (closer to $140).

Per an FT article, “Don Rissmiller of Strategas recently pushed his odds of a 2026 recession to 35 per cent (in a normal year, he puts the odds at 15-20 per cent). He’s worried not because energy is a big part of the US economy; it isn’t. Nor is it that the US economy is already weak; that isn’t exactly true, either. Instead, what worries him is that important parts of the economy — namely, employment and credit performance — are volatile.”

Rissmiller mentions the weak employment picture, and here it is important to consider AI. The spending by hyperscalers on chips and data centers has to ultimately be justified by some sort of revenue. That revenue would come from users of AI, who look to AI for higher productivity and/or reduced expenses. The latter has real world consequences. So far, as mentioned, the data is not supporting significant job replacements by AI, though Boston Consulting Group states, “While job augmentation and new-job creation will happen rapidly, full substitution of jobs by AI will be slower. Five years from now—or perhaps further in the future—10% to 15% of jobs in the US could be eliminated.” This is the type of future Vonnegut envisions in Player Piano, albeit at the extreme.

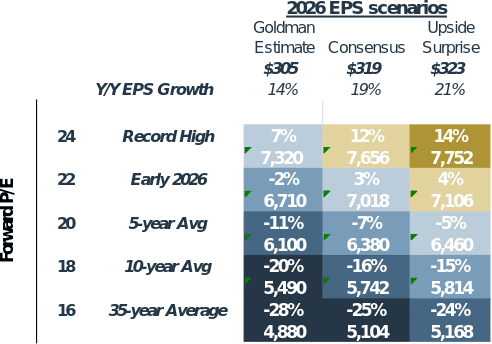

As we started the year, the pathway to sizable market gains seemed challenging, given elevated multiples. Multiples have come down, and earnings growth has been strong. However, at the index level, meaningful gains are predicated on earnings meeting (or exceeding) already lofty expectations, and multiples re-expanding back toward record levels. Both of those things seem less likely unless the geopolitical situation (and accompanying higher inflation and interest rates) is resolved relatively quickly. According to J.P. Morgan, “if $120 oil were sustained for 6 months, annual S&P 500 EPS estimates would decline by $12.7 or 4% of consensus EPS of $317 per share”; this would put us at the Goldman Sachs $305 EPS estimate.

Source: Goldman Sachs, FactSet; as of April 10, 2026

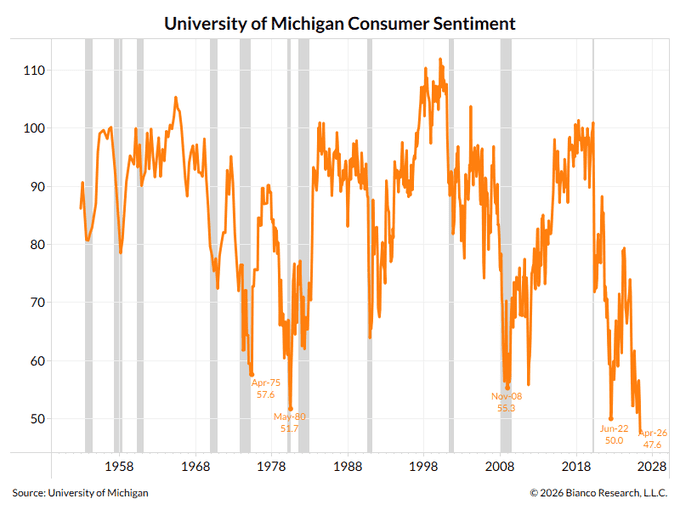

While EPICAC, the supercomputer running the economy in Player Piano’s America cannot feel, people, including investors, do, and they have never felt worse. In the almost 75-year history of the University of Michigan consumer confidence index, there has never been a lower reading. Never. Despite this unease, the manic market posted back-to-back 3% weekly gains since the 3/31 de-escalation that preceded the ceasefire.

We once tasked Claude to write a newsletter, it put EPICAC, the supercomputer housed in Carlsbad Caverns that “contains enough wire to reach from here to the moon four times” on the banner. It was said it “could consider simultaneously hundreds or even thousands of sides of a question utterly fairly, that EPICAC XIV was wholly free of reason – muddying emotions, that EPICAC XIV never forgot anything – that, in short, EPICAC XIV was dead right about everything.”

Many advocates have similar views about AI. And yet, as we reviewed the newsletter Claude wrote, we found myriad errors.

For example, we alluded earlier to Microsoft’s sharp share price decline in Q1 (worst among the Mag 7 and largest detractor to S&P 500 in Q1), and yet Claude deemed Microsoft’s market signal “Optimal”. Claude stated the S&P 500 was “near-flat for the quarter”; it declined over 4%, though later it stated “S&P 500’s historical record after a negative first quarter is actually mostly optimistic”, a clear contradiction. In a six-page newsletter, Claude made ten (10) inaccurate statements about financials markets/companies, had three (3) poorly conceived references to the novel, and made at least five (5) syntactical errors.

Importantly, while EPICAC may be free of emotion, current AI tools are not. Are they designed to be objective arbiters of facts, or to keep users engaged? Based on our experiences thus far, it seems to be the latter. We have found that these tools are often serving as more of an echo chamber as opposed to an objective analyzer of data.

Which brings us to our role as your financial advisor. In an age where volatility is elevated, misinformation is widespread, and AI tools provide either bad information (our Microsoft example) or self-reinforcing feedback (be it bullish, bearish, or apocalyptic, depending on what ChatGPT or Claude thinks you want to hear), objective advice and guidance have never been more important.

Over the last few years, some of our clients have asked why they should own anything except the winners, i.e., the Magnificent Seven. Claude might have said go for it.

Vonnegut writes, “People are finding that, because of the way the machines are changing the world, more and more of their old values don’t apply anymore.” We agree that machines are changing the world. Algorithmic trading, AI-driven investment “research”, robo-investing: all of these things are changing how the market moves. However, just because some of the old values do not apply, does not mean none of them do. We prefer to be a human voice of reason and objectivity in a world of hyperbole and misinformation, and we continue to see merit in the values of diligent investment research, a long-term approach to portfolio management, and personalized guidance and planning.

Part III: In-depth analysis of Key Factors

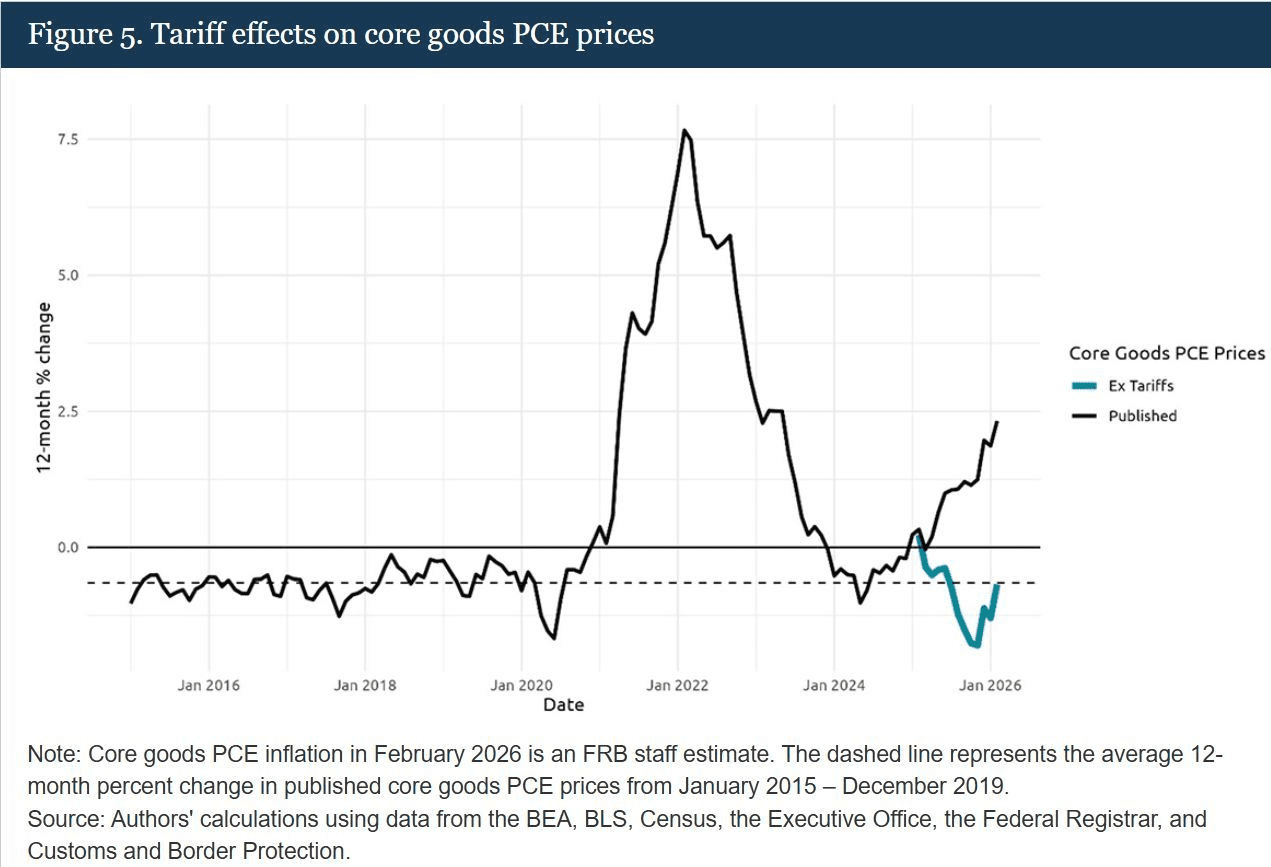

- Inflation – Negative and deteriorating. After largely made-up data for Q4 (government shutdown), the inflation picture has deteriorated. Is the Fed serious about inflation? Read this from the Fed’s minutes and be the judge, keeping in mind inflation has been above two percent for five years now: “The vast majority of participants noted that progress toward the Committee’s 2 percent objective could be slower than previously expected and judged that the risk of inflation running persistently above the Committee’s objective had increased.”

Goods, which had seen deflation, are now moving higher, in no small part due to tariffs. Services excluding housing are running over 3% and inflecting higher. As the Inflation Guy Mike Ashton notes, “there’s also a signature here of a turn back higher in inflation.”

- GDP Growth – Neutral and deteriorating. From the BEA: “Real gross domestic product (GDP) increased at an annual rate of 0.5 percent in the fourth quarter of 2025 (October, November, and December), according to the third estimate released today by the U.S. Bureau of Economic Analysis. In the third quarter of 2025, real GDP increased 4.4 percent.” Forecasted growth is expected to be only slightly better (around 1% to 2%) but does call into question the ability of companies to achieve earnings projections (more on that later).

- Fed Policy – Neutral but deteriorating. At the start of the year, a rate cut (perhaps even multiple cuts) for 2026 was considered a fait accomplish with a new, administration friendly, i.e., dovish, Fed Chair taking the helm in May. However, those odds fell sharply with the rise in oil prices. The ceasefire has improved odds of a cut; per CNCB, “Odds for a reduction jumped Wednesday morning, hitting about 43%, according to the CME Group’s FedWatch tool.” However, the chance is below 50%, which is why we move this to deteriorating.

- Interest rates – Negative but stable. At around 4.3%, the 10-year yield is above where it started the year, but only modestly. While 10-year yields tumbled below 4% as a knee-jerk safety trade in the aftermath of the initial strikes on Iran, concerns over inflation (and the U.S. debt) have kept rates elevated. Without relief, mortgage rates will stay elevated.

Source: FactSet

- Credit spreads – Negative but stable. A reminder we use this as a contrarian indicator. In other words, if we see spreads widening into the area above the green line, we may start to view risk/reward more favorably. Both high-yield spreads and investment grade spreads remained near record lows at the end of Q1. Despite myriad headlines regarding cracks in private credit, there remains little concern over public credit.

Source: FactSet

- Stock multiples – Negative but improving. After peaking at over 23x in Q4, multiples have compressed as the index has fallen slightly, and earnings have grown significantly. At around 19x forward earnings, markets are now less than one standard deviation expensive versus their historical norms. If we look at valuation by sector, every S&P 500 sector (except real estate) still trades above its 20-year average.

Source: J.P. Morgan Guide to the Markets

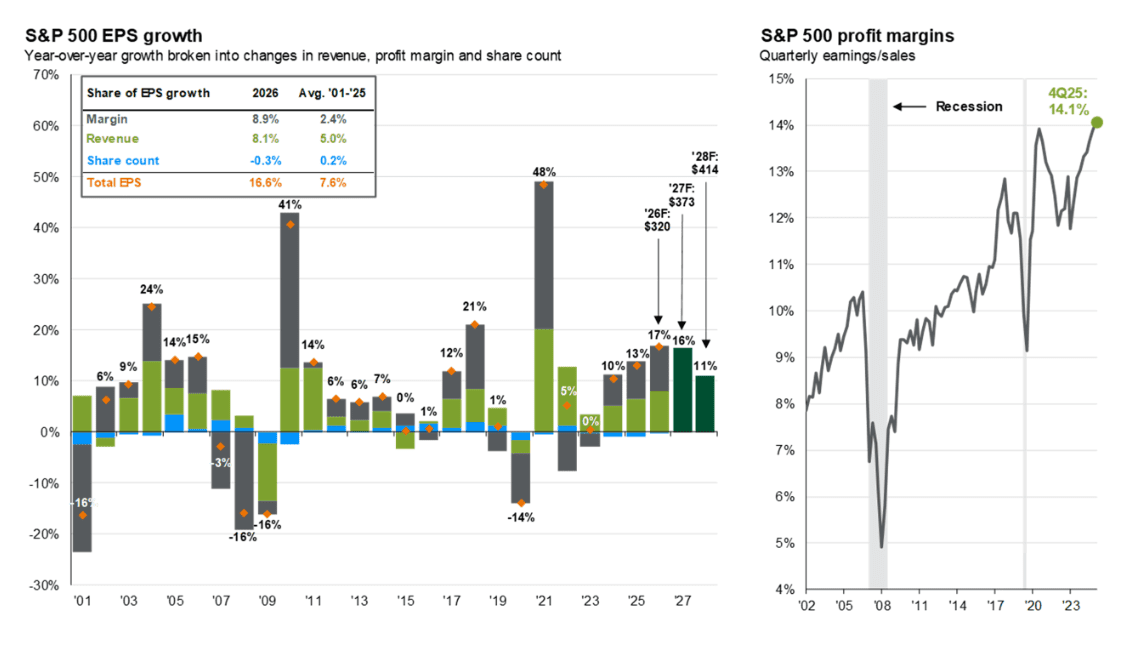

- Earnings growth – Positive and improving. Earnings growth is expected to continue to outpace its historical average. Per the FT, “Analysts expect first-quarter earnings growth to be strong. The forecast for the S&P 500 index (as compiled by FactSet) is for 13 per cent earnings per share growth. The optimism does not end there. Growth for the second, third, and fourth quarters of this year is expected to come in at 19, 21 and 19 per cent, respectively. If that’s right, 2026 earnings growth will accelerate significantly relative to the past several years.” Margins have remained at peak levels and contributed more than ½ of EPS growth in 2026. Whether record margins can be sustained as GDP growth wanes and inflation runs above average is a key question.

READY TO TALK?