Batteries, Lithium, and Lithium Americas

Will Brown

CEO/Managing Partner

Adam Eagleston, CFA

CIO

What You Need to Know About Batteries, Lithium and Lithium Americas1

The U.S. consumer, and the market and investors, have all demonstrated an appetite for environmentally friendly electric vehicles. While the (in)famous companies like Tesla and Nikola garner the most attention, neither company will continue to produce a viable product without access to integral battery components like lithium. Who is most likely to fill their needs?

Battered on Battery Day

Current events dictate a little background before we dive into our analysis of Lithium Americas.

Misdirection is an entertainment and showmanship strategy employed by, most notably, P.T. Barnum. Recently, showmanship had been in vogue, but it has its pitfalls, as infamous former Nikola (NASDAQ: NKLA) Chairman Trevor Milton can attest. We, at Formidable, believe that Elon Musk, darling of Tesla (NASDAQ: TSLA) and SpaceX, witnessed Milton’s recent Icarian descent, and promptly decided that there were 420 ways not to fly too close to the sun, which made the much hyped September 23, 2020, Battery Day a flop, at least judging by the reaction of not just Tesla’s stock price but that of the entire electric vehicle complex. Seemingly everyone was battered on or around Battery Day

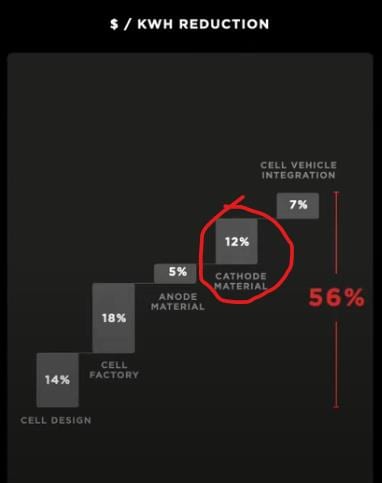

We believe his goal was to obscure that Tesla failed to announce any new imminent efficiencies. In fact, they stated that they were “multiple iterations from having a new battery.” This is seemingly code for, “we’re not there yet, but we have to say something because our stock is going to be hammered if we don’t.” The timeline for the improvements in range and reductions in cost were between one and three years in the future.

Musk also promised a $25,000 Electric Vehicle that will be made available to the public in three years; even a cursory inspection of the historical records indicates the same “in three years” timeline was outlined in first 2018. On an inflation adjusted basis, that would equal, in today’s dollars, about

$23,500. We have seen this before. This is astonishing and should worry Tesla’s faithful, because, currently, the average price of a new car is about $36,000. Hmmm….wrong direction, misdirection, no direction ….we don’t know, and that is a problem.

Our guess is that Musk’s rather robust risk management and legal team realized that Nikola’s Trevor Milton’s recent egregious puffery could draw regulatory scrutiny to Musk’s statements (conspicuously absent was any mention of the million mile battery) on Battery Day, which has now turned out for shareholders, to be just that…although the different definition of battery. The realities are that Tesla is multiple iterations from getting this right. They don’t have what they need, and it has neither been perfected or invented, so this apparent misdirection was their only move. Seeing the market’s response is nonsensical and fashionable. Musk may become alarmed when he saw the DOJ and SEC put the turn the screws on Milton and Nikola.

We have no problem with Tesla as a company, and we believe that they are a transformative innovator technology company with an army of highly intelligent people. That said, we also believe its self-inflicted Battery Day lacked in substance and was an unusual unforced error. Relegated to this outcome of supposition and pseudo data sharing, Tesla and Elon Musk were seemingly cornered into an Asymmetric Dead End.

However, Musk’s comments about the use of lithium during Battery Day were P.T. Barnum-esque. Tesla’s new deal (not announced at Battery Day but concurrently) with fledgling North Carolina-based (though Australian-owned) Piedmont Lithium (NASDAQ: PLL) is seemingly nothing more than misdirection. It’s also likely not a great deal for PLL since it’s fixed price, not to mention conditional.

Musk’s message seems to be, “lithium bad…sell lithium,” yet it appears that Tesla is going to go into the lithium mining and cathode business in Nevada? That is an interesting contrast behind what they say and what they do.

Moreover, while most of Battery Day seemed well rehearsed, the lithium piece was somewhat slapdash, demonstrating a lack of understanding. Based on Musk’s analysis of the lithium mining process it sounds like anyone could walk outside, find some lithium, dump table salt and water on it, and, presto, become a supplier. Voices of reason disagree, including Joe Lowry, who does a wonderful podcast on all things lithium2 and probably first made the Elon/P.T. comparison:3

Showmanship is not the same as innovation. Nothing has changed. The lithium miners will still face geometric upside demand for their products in the months, years, and decades to come, whether from Tesla, upstarts with products not reliant on gravity for propulsion, or established automakers intent on grabbing share. Wall Street and the herd of sheep listening to their “after the house has burned to the ground shouting “fire!”” analysis is what we have all come to expect. Nothing…. nothing has changed in the lithium space; the only noise around it is the sound of the air coming out an event.

With the pressure increased and scrutiny high, Musk qualified cost reductions by stating “…probably to fully realize the advantages it’s three years or thereabouts.” Even if President Donald Trump compares you to Thomas Edison and says “we have to protect our genius,” if our genius wants to mine lithium in Nevada, he has to go through a process that takes a heck of a lot longer than three years. So either, a) these cost reductions won’t be achieved (possible), or b) Musk’s statement that Tesla, “got rights to a lithium clay deposit in Nevada…over 10,000 acres” is a reference to Thacker Pass (much more on it later).

This leads us to a deep dive on the value of Lithium Americas (NYSE: LAC), which is on sale thanks to Battery Day, and maybe that’s what Musk wanted. Is it possible for Musk to claim to have 10,000 acres (no record of that; no permits filed), a magical process for extracting lithium unknown to any other lithium experts, convince a small player into a poor offtake agreement, and torpedo the prices of lithium and its miners so he could drive a harder bargain with a company that actually has the necessary resources?

Lithium Americas: Preposterous Valuation and Prime Location Make This a Compelling Name

Preposterous, from an etymological perspective, means to put the beginning before the end. It seems like our research at Formidable in the green energy/electric vehicle space has worked this way. Beginning with Workhorse (NASDAQ: WKHS), a manufacturer of vehicles, then going to battery technology with Nano One Materials Corp (OTCMKTS: NNOMF) (as a sidebar, much of Tesla’s Battery Day commentary was proof of concept for Nano One’s battery technology), we now find ourselves at the beginning of the supply chain: the producers of the raw materials that go into the batteries that power the vehicles. In this case, the lithium at the heart of the chemical processes.

We are just as dubious as anyone else when it comes to owning commodities-oriented businesses. They tend to be capital intensive, highly regulated, and a victim of the reflexive nature of commodity cycles. One need look no further than the carnage in the U.S. shale industry to understand what the combination of cheap capital and a commodity cycle can do to share prices.

However, we believe we have identified a differentiated operator in the lithium space in Lithium Americas (NYSE: LAC; TSX: LAC). Formidable Asset Management (“Formidable”) recently established a position; and the following are the key pieces of our investment thesis behind this action:

- Imminent Production

- Strategic Location

- Undervalued Assets

Overview

Lithium Americas is based in Vancouver, Canada, though the stock is dually listed in both the United States and Canada. The company is developing two lithium mines: one in Argentia and the other in the United States.

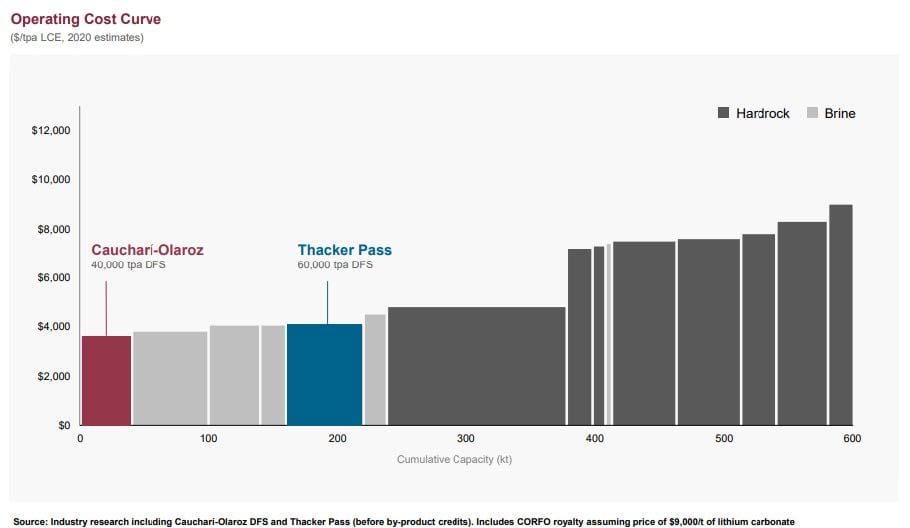

LAC’s joint venture with Ganfeng Lithium, Minera Exar, aims to produce 40 ktpa from the Cauchari-Olaroz site, located in western Argentina. Work on the project began in 2017 and relies on extracting lithium from brine. LAC’s Thacker pass is estimated to be able to produce 60 ktpa and uses material sourced from an open pit mine. Over 50% of the total reserves for the company are relatively cheap on the cost curve:

Approximately 30% of the company is owned by two large foreign entiries: China’s Ganfeng Lithium and Thailand’s Bangchak Corp. Insiders and directors own over 12%.

Imminent Production

While LAC is moving forward with its plans to bring the Cauchari-Olaroz site online, major competitors like Chile’s SQM (NYSE: SQM) and U.S.-based Albemarle (NYSE: ALB) and Livent Corp. (NYSE: LTHM), on recent earnings calls, announced reductions in capital spending. The project has seen setbacks due to COVID restrictions, though construction is over 45% complete. Best guess is that, barring unforeseen setbacks, the mine should be producing by the end of 2021.

The timing may be perfect. Even before the announcements, research from Cannacord estimated 450kt of lithium carbonate equivalent (LCE) had been removed from the global lithium pipeline since August 2019.

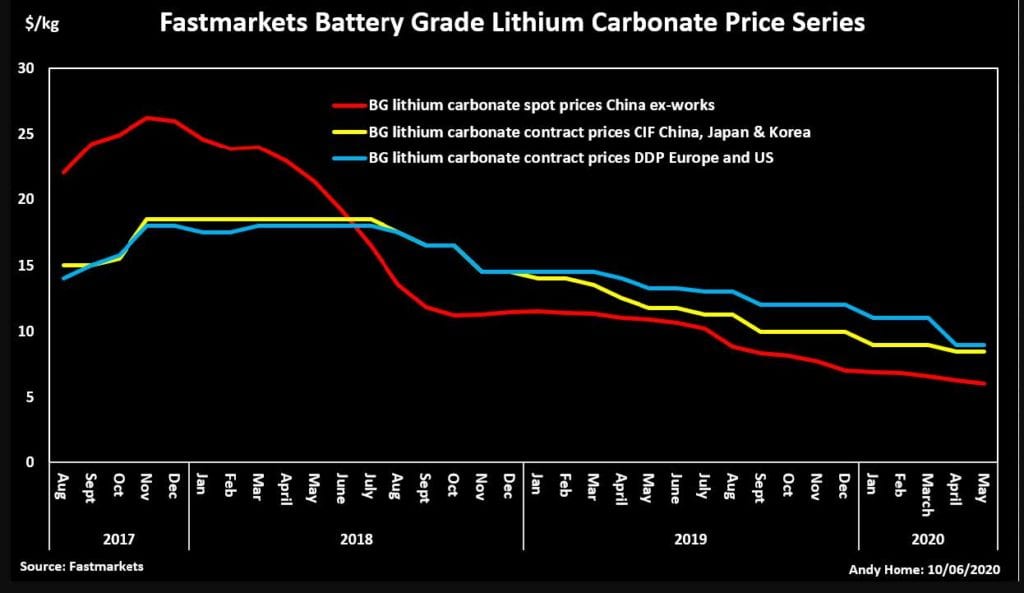

One reason is that, unlike other commodities, there is not currently a functioning futures market for lithium4. Per Reuters, even spot pricing is “opaque and fractured5”, and individual end clients required bespoke products, i.e., lithium is less of a commodity in the traditional sense, which is a positive for LAC. However, this inability to hedge produces wilds swings in price, affecting capex decisions and leading to the boom/bust cycle that has plagued lithium.

The company’s assumptions for Cauchari-Olaroz use $12k per ton as the price for lithium carbonate, which is well below the peak of $17k in 2018 though above current spot rates, which have been impacted by COVID.

Like the metal itself, prices for lithium are volatile, and the reflexive nature of commodities prices are likely to give a bid to lithium over the coming years. The supply chain for lithium mining is relatively long, so prices tend to overreact on both the downside and upside, making LAC’s investment in the teeth of a challenging price environment a good contrarian bet. According to Emily Hersh, managing partner at US consultancy firm DCDB Group, in the short term the market will face oversupply, but a lower supply scenario is expected in 2023-25 due to the lack of financing to build new projects or expand those that exist.6

Strategic Location

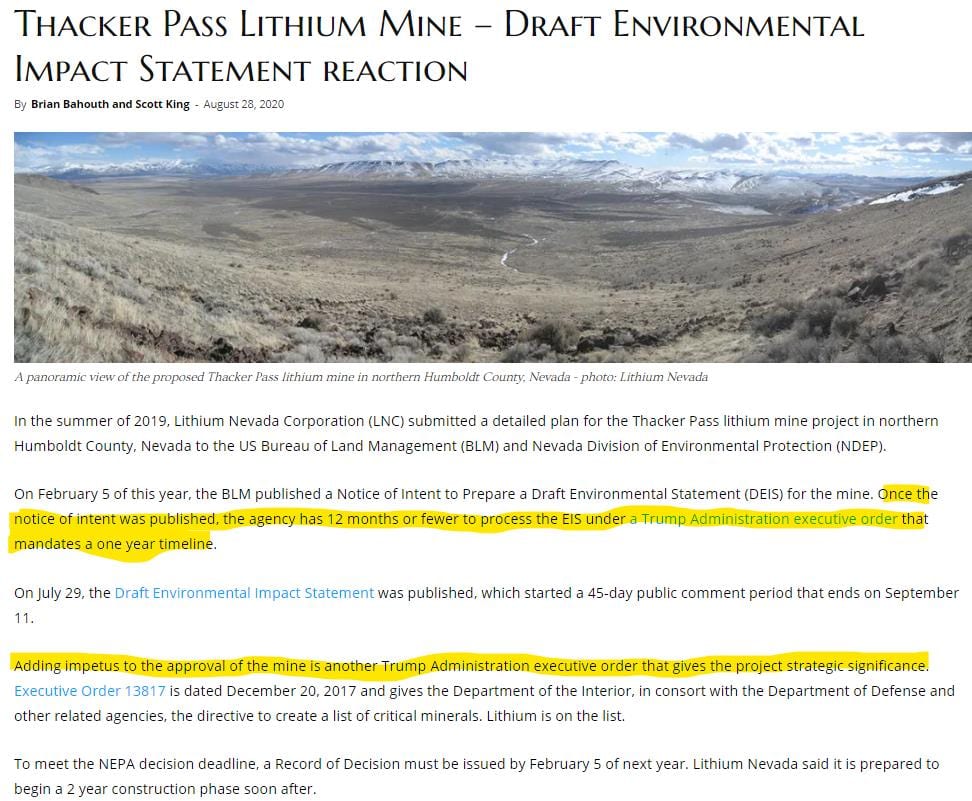

Argentina is not exactly a hotbed of electric vehicle production, nor is it the most stable political or economic regime. On the other hand, LAC’s Thacker Pass mine is in the United States; Nevada, to be more precise. Approval of the site is not a fait accompli. A draft Environmental Impact Statement was published July 29, 2020.7 A Definite Feasibility Study is due in Q4 on what is the largest known lithium resource in North America.

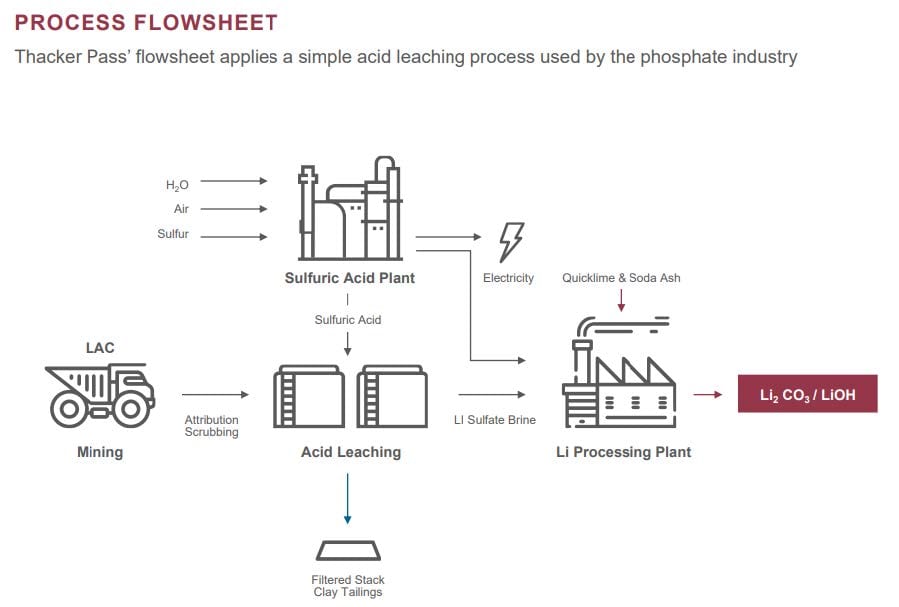

Relative to Cauchari-Olaroz, Thacker Pass can be brought online in a shorter period of time, i.e., within two years of the start of construction. The former, as mentioned, uses a traditional brine extraction process. Thacker Pass uses the following process, which uses open pit mining (not the greenest thing in the world, we know):

Setting aside the quicker timeline, the most compelling thing about Thacker Pass is its location. There are two main considerations here: one economic, one strategic.

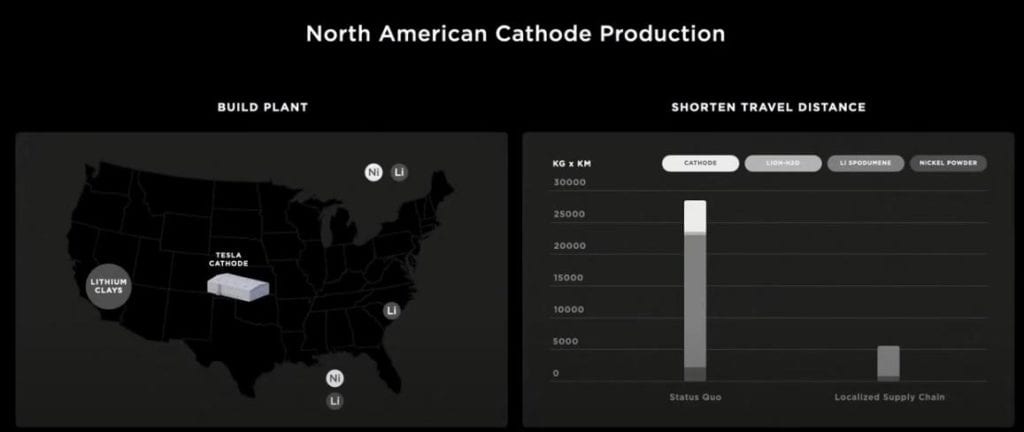

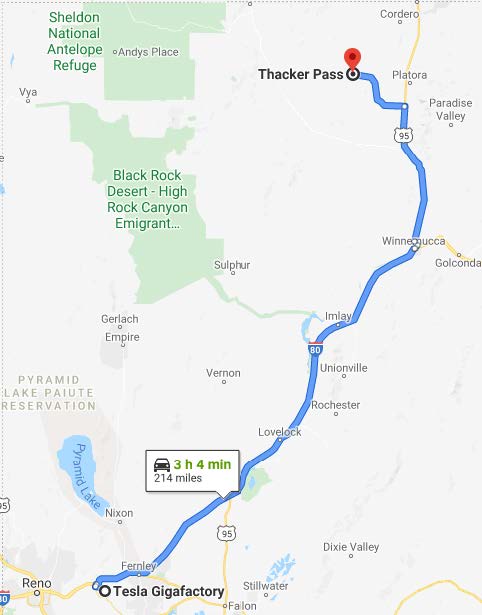

In the case of the former, proximity to end users provides an economic advantage for commodity producers, given transportation cost is a key component of price. Tesla (NASDAQ: TSLA) located its Gigafactory 1, a lithium-ion battery and vehicle factory near Reno, Nevada.

In the case of the latter, as a result not just of COVID but other strategic and security concerns, there is an increasing emphasis on sourcing inputs nearer to home to develop a more resilient supply chain. Cathode and anode production is dominated by Asia, especially China. Lithium supply is dominated by South America and Australia, with the former exposed to political risk. One need look no further than recent headlines, when SQM had operations halted in its home country.8

Politically speaking, the drive to encourage domestic production of “strategic metals” has come from the Republican party on defense grounds, i.e., to eliminate dependence on China. However, the prospect of any Green New Deal promoted by the Democratic party will ultimately, we believe, compel environmentalists to acknowledge what Benchmark Mineral Intelligence Managing Director Simon Moores, a global authority on lithium-ion batteries supply chains, told the resources committee, specifically “We are in the midst of a global battery arms race in which the U.S. is presently a bystander,” and “Those who control these critical raw materials and those who possess the manufacturing and processing know-how, will hold the balance of industrial power in the 21st Century auto and energy storage industries.”9

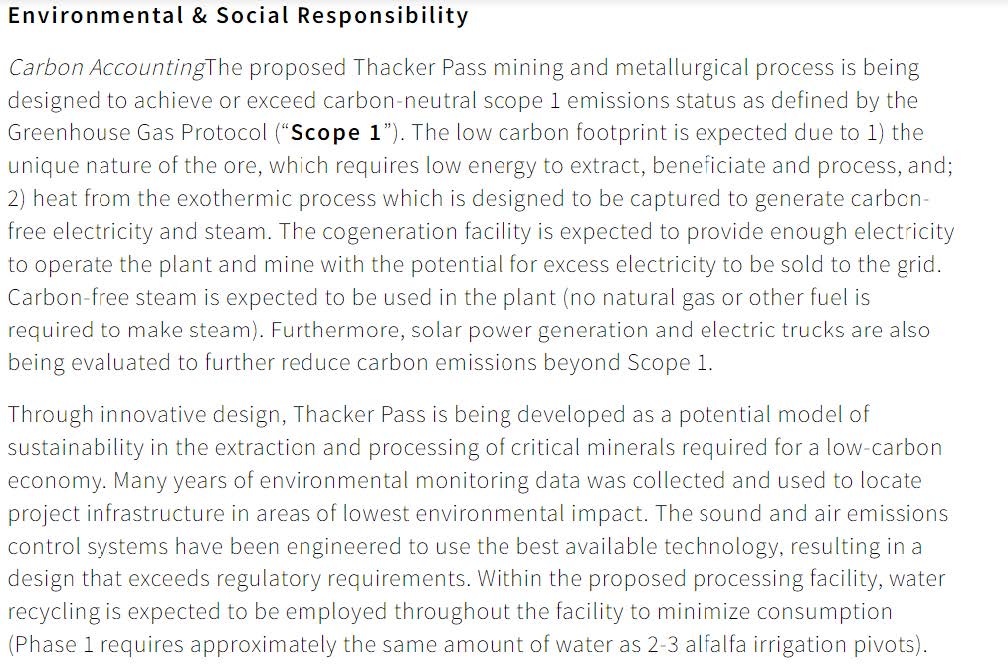

Open pit mining in Nevada is probably not high on the list of environmentalists, but in this case the ends may justify the means. Moreover, cognizant of these concerns, Thacker Pass is designed to be environmentally friendly:

Undervalued Assets

We will delve into specifics in the valuation section, but suffice it to say based on the valuation of its competitors (relative to their potential production/earnings) as well as recent prices paid for assets by its competitors, LAC’s current market cap is well below what we believe the value of its assets to be.

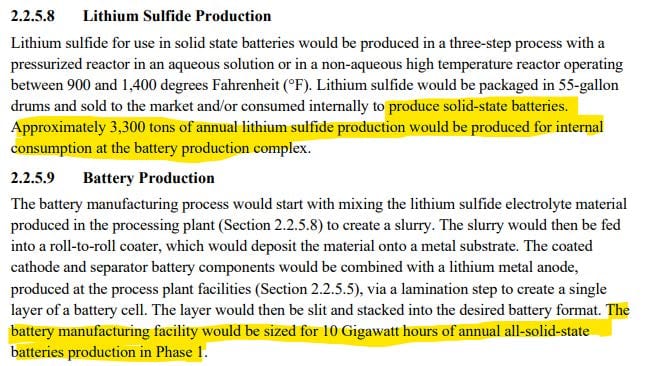

Given the secular tailwinds for electric vehicles and the corresponding demand for lithium, such a mispricing is unlikely to persist. Moreover, the company’s Draft Environmental Impact Statement, dated July 31, 2020,10 contained the following nugget of information (emphasis ours):

There are three huge takeaways. One, this is no simple lithium mine but a battery manufacturing facility as well. Two, the quantity of batteries is not insignificant. For sake of comparison, Tesla’s Gigafactory has about 35 Gigawatt hours of capacity currently, enough to produce 500k battery packs, which is not enough to produce the volume of cars the company hopes. Third, LAC is going to be making solid-state batteries, which are the key to things like the mythical million mile battery.11 Given this foray into batteries and the fact that both LAC and Nano One are located in Vancouver, could this be a match made in heaven?

If, as bulls might say, Tesla is a battery company, not a car company, then ascribing a value to LAC’s battery operation produces a valuation well in excess of anything we might envision.

Valuation

The most salient valuation methods for LAC are comparisons with competitors, both in terms of their existing valuations versus LAC as well as prices recently paid for other lithium assets; discounted cash flow analysis also offers a valid framework.

Comparable M&A

U.S.-based Albemarle (NYSE: ALB) paid $1.15 billion in December 2018 to Mineral Resources Limited (ASX: MIN) for a 50% interest in its Wodgina Project. The project is anticipated to produce 100 ktpa of lithium carbonate equivalent (LCE), though the division into two stages of 50 ktpa each seems to indicate some difficulty in extracting the second half. The project uses spodumene, which is mined from hard rock as opposed to being produced from brine; some consider the spodumene approach superior, given it uses fewer steps, so a premium from a valuation perspective was warranted. The effective price per ktpa (kiloton per annum) was $23 million.

If we use a similar framework for LAC, we derive a value of $450M for Cauchari-Olaroz and $1.4 billion for Thacker Pass, for a total of $1.8 billion. If we discount the former for its use of brine (we have seen brine given as much as a 50% discount) we still get an equity value of $1.6 billion. Albemarle’s transaction was at a time when spot lithium prices were much higher; approximately 50% greater than today. Applying such a discount still yields a valuation of $800M, above LAC’s current market cap.

Pure Play Competitor

Though SQM and LAB are the largest players, neither is a pure play in lithium. Domestically, Livent

(NYSE: LTHM) is the closest thing to a pure play. Looking simply at its capacity per its 2019 annual report, we see around 55 ktpa; the breakdown between performance and base is roughly even. Given its market cap of $1.1 billion, the implied market cap for LAC, given its production capacity, would be $1.6 billion (LAC’s current market cap is $640M).

Net Present Value

A little more dubious but worth the exercise is an attempt to calculate an NPV for the company’s assets.

We used the following assumptions:

- Cauchari-Olaroz begins production at the end of 2021

- Thacker Pass begins production at the end of 2023

- Company’s cost curve is accurate

- Low cost regime last for 60% of useful life

- High cost regime for remainder

- 40-year useful life

- Tax rate of 20%

- Weighted average cost of capital of 15% (considers higher risk profile of mining)

At the company’s projected lithium price of $12k, we get an NPV for Cauchari-Olaroz of $618M, with Thacker Pass at $1.4 billion; total is approximately $2 billion, or around $22 per share. The company’s estimate of $12k is not too different than the average price over the last year, though clearly that average does not reflect the large swings we have seen. There is a reasonable chance that the company introduces a joint venture partner for Thacker Pass. If we assume that occurs (and that LAC retains 50%), we get a price of approximately $15 (over 100% above its 9/23/2020 close).

Were we to use current spot, which we believe are extremely depressed, we would get a market cap of approximately $605 million for the company as a whole. Conversely, at peak prices (approximately $16k), we get a total market cap of just over $3 billion.

With 90 million shares outstanding, we estimate a fair value between $15 USD and $22 USD, 110% and 220% above the stock’s closing price on September 23, 2020, respectively.

Importantly, this excludes the market re-rating LAC as a battery company as opposed to simply a lithium miner.

Lithium Americas’ Challenges

As stated at the outset, this is a commodities business from a perception perspective at a minimum. Though the company has strategic advantages in terms of proximity of its Nevada location, the globalprice for lithium will affect its revenues. Currently, the market is oversupplied, and projections from some on the sell side see a glut for the foreseeable future.

Risks exist for both projects. As stated previously, Argentina’s political and economic situation is not the most stable. Additionally, partner Ganfeng owns 51% of the venture and, as a Chinese company, is entangled with the Chinese government from a governance perspective. Approval from the Chinese government was required for recent financing to be approved. It also likely precludes Ganfeng as a potential joint venture partner for Thacker pass, though other entities are likely to have a high degree of interest.

What could unlock the value?

Formidable believes any of the following events could help the market begin to close the gap between LAC’s current price and our estimates of fair value. Each event has a reasonable probability of coming to fruition:

- Favorable legislation – The possibility of a “Green New Deal” is being widely discussed as part of the Biden campaign. Government programs at aimed reducing emissions and incentivizing the shift to EVs would also be a positive for LAC. In the event of a Republican victory, strategic concerns may provide additional impetus to domestic production.

- Spotlight on supply constraints – Despite the puffery at Tesla’s battery day, lithium is a potential chokepoint for achieving the vision many have for renewable energy, LAC is in a prime spot, both from an industry perspective as well as geographically.

- Approval of Thacker Pass – Perhaps the market is ignoring the company’s battery potential as it is just that: potential. Approval of the plan, including the proposed battery facility, may be a transformative event, and the clock is ticking.12

Conclusion

Formidable believes the market has a tremendous appetite for electric vehicles, as do investors. While the OEMs like Tesla may get the attention, they have no product without access to integral battery components like lithium. Despite current weakness, the supply/demand dynamics for the lithium market appear favorable over the coming years, and LAC appears well positioned to take advantage. Moreover, even at “normal” lithium prices, the company is being given almost no credit for its Thacker Pass opportunity, which has the potential to be twice as valuable as its Argentinian operation.

Footnotes

1 – NYSE: LAC; TSX: LAC.

2 – See https://anchor.fm/globallithium, accessed September 24, 2020.

3 – See https://www.reuters.com/article/us-tesla-batteryday-lithium-idUSKCN26E3G1. accessed September 24, 2020.

4 – Home, Andy; Lithium—The Metal of the Future with a Futures’ Problem, published June 10, 2020 and access via URL on September 24, 2020: https://www.reuters.com/article/us-metals-lithium-ahome/column-lithium-the-metal-of-the-future-with-a-futures-problem-andy-home-idUSKBN23H2B8.

5 – Id.

6 – Bnamericas; Lithium Market Weakness Exposed By COVID-19; published June 11, 2020; accessed September 24, 2020 via url: https://www.bnamericas.com/en/features/lithium-market-weaknesses-exposed-by-covid-19.

8 – https://www.reuters.com/article/us-chile-lithium-sqm-idUSKCN25A2PB

9 – https://www.miningnewsnorth.com/page/us-leaders-address-critical-minerals/5742.html.

10 – https://eplanning.blm.gov/eplanning-ui/project/1503166/570

DISCLOSURES

General Firm

Formidable Asset Management, LLC (Formidable) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, Formidable cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of Formidable and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Any index performance cited or used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. The performance shown may not reflect a Formidable portfolio.

Past performance is no guarantee of future results.

Reader should assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies discussed in these materials) made reference to directly or indirectly in these materials will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results.

Specific Securities

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation by Formidable. The specific securities identified and described above do not represent all of the securities purchased and sold for the portfolio, and it should not be assumed that investment in these securities were or will be profitable. There is no assurance that the securities purchased remain in the portfolio or that securities sold have not been repurchased. Charts, diagrams and graphs, by themselves, cannot be used to make investment decisions. You may contact Formidable Asset Management, LLC for a full list of recommendations made during the preceding period one year

Not an Offer

These materials do not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service by Formidable or any other third party regardless of whether such security, product or service is referenced here. Furthermore, nothing in these materials is intended to provide tax, legal, or investment advice and nothing in these materials should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Formidable does not represent that the securities, products, or services discussed here are suitable for any particular investor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation.

The opinions expressed here are those of Will Brown and Adam Eagleston are not intended as investment advice. They are also subject to change with changing market conditions. Clients of Formidable may have positions in securities discussed in this article. This writing is for informational purposes only—Formidable and the authors expressly disclaim all liability in respect to actions taken based on any or all of the information from this writing.

READY TO TALK?