Will Brown

CEO/Managing Partner

Adam Eagleston, CFA

CIO

Jacob Fry, Research Analyst

Flux Power Holdings Update: Financing and Valuation

Executive Summary

Our previous article on Flux Power Holdings, Inc. (NASDAQ: FLUX) could not have been much more poorly timed. Days after our report, on September 22, 2021, the company reported its financial results for Flux’s fourth quarter (Q4 ’21) and fiscal year (FY ’21) ended June 30, 2021. These results included another quarter of record sales growth and an impressive $18 million backlog. However, the next day (September 23, 2021), the company announced a capital raise that we found vexing, given the company’s untapped line of credit provided ample capital to fund its current working capital needs.

Though we were disappointed in the raise, the market reaction was disproportionate to the magnitude of the event, and the valuation discrepancy we highlighted has since become even larger.

Flux Power Holdings Update: Financing and Valuation

In the following, we will provide an overview on the capital raise, explore an overlooked structural factor that explains some of the price reaction, and estimate where we think fair value for the company is now. As a reminder, we first wrote about FLUX on November 5, 2020, when the stock was trading at a 3.5 price/sales multiple (NTM). On September 9, 2021, the stock was trading at a 3.0 forward-looking price/sales multiple. As of October 21, 2021, it stands at 2.6.

Trading at its own historical price/sales ratio would put the stock at approximately $8, whereas even at a 50% discount to its peers, the stock would be just over $20 per share.

| P/S vs. 2022 Revenue ($M) | 30 | 34 | 40 |

| 3 | 5.30 | 6.00 | 7.06 |

| 4 | 7.06 | 8.01 | 9.42 |

| 5 | 8.83 | 10.01 | 11.77 |

| 7 | 12.36 | 14.01 | 16.48 |

| 10 | 17.66 | 20.01 | 23.55 |

| 15 | 26.49 | 30.02 | 35.32 |

Capital Raise

The company used its existing shelf registration to sell securities to several institutional investors on September 27, 2021, which included 2,142,860 shares of stock and warrants to purchase up to 1,071,430 aggregate shares of common stock at a purchase price of $7 per share and associated warrant, were sold at $7 per share. The warrants had an exercise price equal to $7 per share, were exercisable immediately upon issuance, and expire five years from issuance.

The gross proceeds were approximately $15 million before offering expenses, which were close to $1 million.

Although framed as a “bought deal,” the market’s reaction was negative, to say the least, with shares falling from around $7.52 (closing price on 9/22/2021, the day the company reported earnings and before the deal was announced) to $4.99 by the close on 9/29/2021, representing a nearly 34% decline.

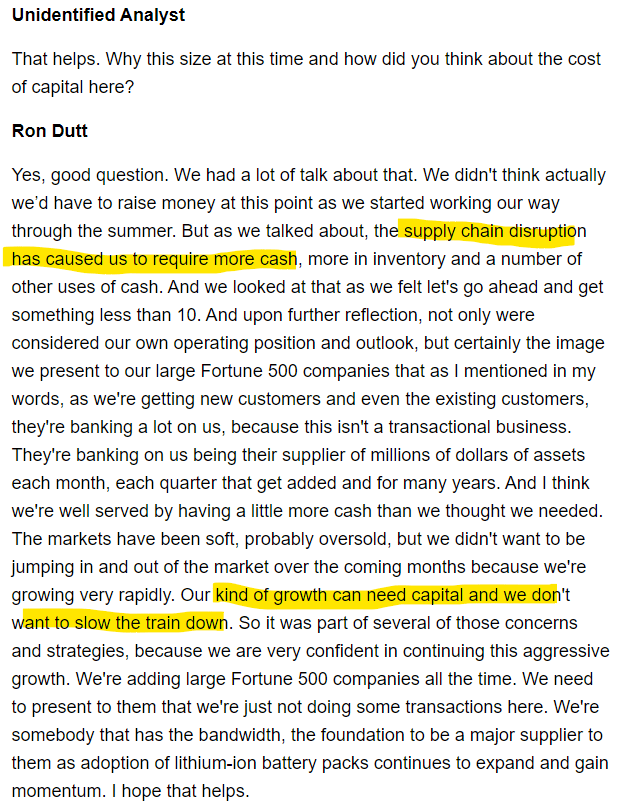

Here is an excerpt from the company’s earnings call explaining the rationale for the capital raise; the “Unidentified Analyst” is one of the authors of this whitepaper:

The reason for our pointed questions on the call is that the company seemingly had cheaper financing options available, especially as it relates to working capital and access to credit to fund inventory needs. However, as CEO Ron Dutt explained, management and the Board believed a more solid cash position on the balance sheet was a prerequisite to continuing to land business from the Fortune 500 companies. Given the stock’s reaction to the deal, the effective cost of capital here was quite high.

Having said that, part of the reason for the decline was less related to the capital raise and more structural in nature. Given we have yet to see sell-side analysts or management address the topic, we thought it important to discuss. For those who follow the stock closely, one of its largest holders was the Invesco Wilderhill Clean Energy Fund (NYSE: PBW). On 9/29/2021, PBW eliminated its entire stake in Flux, which was a little over one million shares. There was not a clear reason per the prospectus, given our review indicated the stock still qualified for inclusion:

However, the Index Provider decided the company should no longer be included in the index (passive funds are sometimes more active than you think). Given average daily volume on FLUX was around 68,000 shares per day, this was simply too much stock for the market to digest (fifteen days or thereabouts) in a single day, especially after the capital raise.

Valuation

Valuing a company like Flux is a challenge. Though at first glance Flux is a mature company, in fact its shift in focus places it more in the emerging growth category. Peers like PLUG, BLNK, FCEL, AND BEEM would qualify as emerging growth, while ENS is a mature, slower growth company, albeit in the battery space. When looking at companies we broadly consider competitors, we see Flux is cheap in terms of price/sales:

| Trailing 12 Month Sales ($M) | Market cap ($M) | P/S | |

| FLUX | 26 | 89 | 3.4 |

| PLUG | (6) | 18,635 | -3324.7 |

| BLNK | 10 | 1,223 | 123.0 |

| FCEL | 73 | 3,083 | 42.4 |

| ENS | 3,088 | 3,316 | 1.1 |

| BEEM | 7 | 263 | 37.9 |

| Average (ex-negatives) | 41.6 | ||

| Median | 20.6 |

| Next 12 Month Sales Estimate ($M) | Market cap ($M) | P/S | |

| FLUX | 34 | 89 | 2.6 |

| PLUG | 616 | 18,635 | 30.3 |

| BLNK | 28 | 1,223 | 44.0 |

| FCEL | 108 | 3,083 | 28.5 |

| ENS | 3400 | 3,316 | 1.0 |

| BEEM | 15 | 263 | 17.5 |

| Average | 20.6 | ||

| Median | 23.0 |

Even if the company trades at its own historical price/sales ratio (approximately 4x), we get a price of $8, approximately 40% above the current $5.70. At 10x sales, a multiple well below the peer median of 23x, we derive a stock price of approximately $20 per share, assuming the company achieves the $34 million in projected revenue for 2022. Our estimates consider approximately one million shares in dilution from the warrants issued as part of the capital raise:

| P/S vs. 2022 Revenue ($M) | 30 | 34 | 40 |

| 3 | 5.30 | 6.00 | 7.06 |

| 4 | 7.06 | 8.01 | 9.42 |

| 5 | 8.83 | 10.01 | 11.77 |

| 7 | 12.36 | 14.01 | 16.48 |

| 10 | 17.66 | 20.01 | 23.55 |

| 15 | 26.49 | 30.02 | 35.32 |

| 20 | 35.32 | 40.03 | 47.09 |

The company’s current stock price is giving it no credit for the growth it has achieved, the strong momentum it is building with high-profile customers, its more diversified product suite, and its progress toward achieving critical milestones. With its capital raise and share overhang from the large ETF holder now in the past, we are optimistic the market may start to awaken to the growth story and valuation discount.

DISCLOSURES

General Firm

Formidable Asset Management, LLC (Formidable) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, Formidable cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of Formidable and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Any index performance cited or used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. The performance shown may not reflect a Formidable portfolio.

Past performance is no guarantee of future results.

Reader should assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies discussed in these materials) referred to directly or indirectly in these materials will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results.

Specific Securities

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation by Formidable. The specific securities identified and described above do not represent all the securities purchased and sold for the portfolio, and it should not be assumed that investment in these securities were or will be profitable. There is no assurance that the securities purchased remain in the portfolio or that securities sold have not been repurchased. Charts, diagrams, and graphs, by themselves, cannot be used to make investment decisions. You may contact Formidable Asset Management, LLC for a full list of recommendations made during the preceding one-year period.

Not an Offer

These materials do not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service by Formidable or any other third party regardless of whether such security, product or service is referenced here. Furthermore, nothing in these materials is intended to provide tax, legal, or investment advice and nothing in these materials should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Formidable does not represent that the securities, products, or services discussed here are suitable for any particular investor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation.

The opinions expressed here are those of Will Brown, Adam Eagleston, and Jacob Fry, and are not intended as investment advice. They are also subject to change with changing market conditions. Clients of Formidable may have positions in securities discussed in this article. This writing is for informational purposes only—Formidable and the authors expressly disclaim all liability in respect to actions taken based on any or all of the information from this writing.

READY TO TALK?