Flux Power Holdings

Will Brown

CEO/Managing Partner

Adam Eagleston, CFA

CIO

Inflection Point for Flux Power Holdings, Inc.1

Sometimes, it is better to be a little boring. Most of the attention in the electric vehicle space is focused on glitterati: the OEMs that make roadsters that go 0-60 in the blink of an eye, the larger-than-life CEOs that tweet incessantly, you get the idea.

We believe we have found a company that has the potential to be just as successful, if not more so. The company’s focus on the less glamorous application of lithium-ion technology, not to mention one where existing, expensive machinery can be retrofitted to reduce downtime and costs, gives the company additional optionality.

We believe we have identified an undervalued company in Flux Power Holdings, Inc. (NASDAQ: FLUX). Formidable Asset Management (“Formidable”) recently established a position2 the following are the key pieces of our investment thesis behind this action:

- Compelling client value proposition

- Sizable addressable market and strong client relationships

- Conversion from product sale to service

Overview

The last five years have catapulted the technology and artificial intelligence revolution into hyper gear. Visionaries such as Isaac Asimov clearly outlined what is now taking shape in our society today, although colonizing Venus may be a way off. Formidable has taken a pole position in several notable investments that derive their value from this revolution.

It is our opinion that society has merely scraped the surface, and through extensive research we have been able to unearth what we believe are significant values that are clearly misunderstood within the electric vehicle ecosystem. To use a baseball analogy, we are not just in the early innings, the players are just now stepping out of the dugout.

This brings us to Flux, a lithium ion battery producer for the myriad day-to-day operating activity within the materials handling sector.

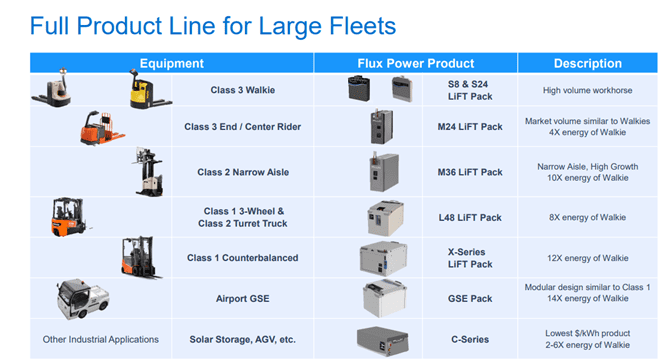

Slide from Flux company presentation accessed on November 4, 2020 via url: https://www.fluxpower.com/hubfs/Company%20Presentation/Flux%20Power%20Company%20Presentation%20-%20October%207,%202020.pdf

While in the early stages of penetration of its main market, Flux has immense opportunities in other industrial segments as well as residential assets such as lawnmowers, portable power packs for military assets, and life supporting rescue assets that are easily mobilized (think pop up mobile hospitals, clinics, disaster relief deployment); the applications for the batteries they produce are nearly endless.

Flux also has burgeoning opportunities to leverage its technology to provide power solutions to rural municipalities for emergency purposes as well as solar electric vehicle charging, which is a true green energy solution.

Compelling client value proposition

We can tout environmental consciousness until we are green in the face, but ultimately customers want products that:

- Limit downtime

- Lower costs

- Are safe

- Are durable

Flux batteries seemingly check all the boxes.

The efficiency of lithium batteries versus lead acid batteries is integral to all four of these attributes. The simplest way to think about this is that for every three lead acid batteries, one lithium battery will suffice. The reason – thermodynamics. Lead acid batteries can only be used for about eight hours at a time; for comparison, lithium batteries can be used nonstop and switched relatively easily. The law of thermodynamics comes in to play because, simply put, forklifts that use a lead acid battery for more than one shift become too hot to operate and can ignite from the chemical exchange resulting from the use of lead acid, i.e., safety is an issue with lead.

Therefore, lead acid batteries operate for a shift, cool for a shift, and charge for a shift; hence, they are in use about 1/3 of the time, i.e., there is a lot of downtime with lead acid. This is extremely impactful for clients that are trying to expand efficiency for a fleet of vehicles, e.g., forklifts, making Flux’s lithium ion battery a better solution.

Small lead batteries last about 18 to 24 months. Similarly,sized lithium batteries last seven years, a threefold improvement in every direction. Large lead acid batteries have a life span of five years while their counterparts in lithium last 10 years. Setting aside the simple durability and longer replacement cycle versus lead, which is one source of cost savings, less frequent replacements of toxic lead means lower cost for clean up and improved safety as well. From the company’s 10-k: “Additionally, the toxic nature of lead acid batteries presents significant safety and environmental issues as they are subject to Environmental Protection Agency lead acid battery reporting requirements, may create an environmental hazard in the event of a cell breach, and emit combustible gases during charging. As a result of the advantages lithium-ion battery technology provide over lead acid batteries…” Labor costs are also lower as there is no battery swapping or watering for lithium versus lead acid.

Flux’s offering is designed to meet Underwriters Laboratory (UL) safety standards, and the company hopes to have completed certification of its entire forklift line-up by December 2020.

We will talk more later about additional opportunities Flux has to monetize its client base, but suffice it to say its complementary suite of products further improves its ability to demonstrate value to clients, not to mention the secular tail winds due to the rise of e-commerce, labor shortages, and rising wages.

Strong client relationships and sizable addressable markets

Original equipment manufacturers (OEMs) are currently Flux’s primary clients. Given that most forklifts are financed, and batteries are a sizable part of the cost, the preference for the end client is to combine the two. Accordingly, Flux has developed a private label version for a top 10 OEM, though it sells to others as well. From the company’s 10-k: “Many of our LiFT Packs have been approved for use by leading industrial motive manufacturers, including Toyota Material Handling USA, Inc., Crown Equipment Corporation, and The Raymond Corporation.”

It also sells direct to larger “institutional” clients and has started working with PepsiCo, which has 50k units, i.e., materials handling vehicles, to convert its entire fleet to lithium ion. The key word here is convert. A lead acid battery can easily be swapped for lithium-ion once the former reaches the end of its useful life. Obviously, not all of a fleet’s existing batteries expire at once and swapping out a functioning lead acid battery is typically not the preferred approach for the customer.

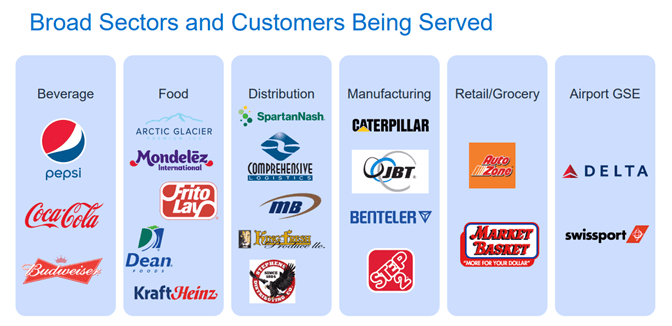

Slide from Flux company presentation accessed on November 4, 2020 via url: https://www.fluxpower.com/hubfs/Company%20Presentation/Flux%20Power%20Company%20Presentation%20-%20October%207,%202020.pdf

Combining OEMs along with the current installed based and we have a compelling driver of value within the company: its addressable market. The company believes that lithium ion currently serves 3% of the battery market. Experts estimate the size of the market at $2.5 billion. As one example, Toyota Industries, Inc., which is the market leader (and a Flux client), is estimated to sell around 250,000 units annually on average over the next three years per Mizuho Securities; it sold 278,000 in FY 2020 (pre-COVID) worth almost $14 billion in revenue, based on exchange rate as of October 19, 2020. That equates to around $50k per unit; lithium-ion batteries average $15-$20k.

According to Modern Materials Handling, the total revenue for the materials handling top 20 manufacturers was approximately $44 billion. Let us assume conservatively that batteries are 25% of the total cost of a forklift. This puts the TAM at around $11 billion for lithium-ion batteries. Obviously, lead acid will continue to have a place due to its lower cost, as will internal combustion and hydrogen (hydrogen is typically used by higher volume players, e.g., Amazon).

The current market penetration for lithium-ion is low single-digits per our conversations with the company and other industry sources. Changing environmental regulations should benefit lithium-ion, and at even a 10% penetration Flux’s TAM is over $1 billion just for the OEM portion of its business.

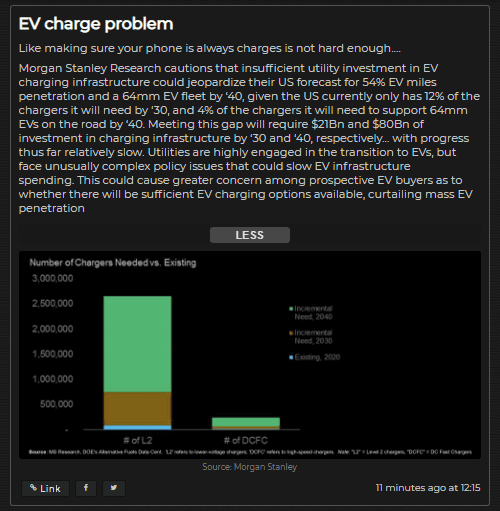

The company’s collaboration with Beam Global (NASDAQ: BEEM) is another huge potential market opportunity in an adjacent space that is currently untapped and has the same secular tailwinds as materials handling. Unlike its peers, Beam provides truly green solutions for charging and power generation, given its use of solar as opposed to fossil fuel or nuclear sources. Flux battery packs store the solar energy for use by electric vehicles, with newer applications being developed for true off-grid power supply for rural areas and/or emergency power generation. As we see from the following, there has been underinvestment in this required infrastructure.

FLUX could be a beneficiary of the confluence of two massive global trends, one secular and one cyclical. The secular is an increased emphasis on EVs; we have talked about this extensively in the past. The second is government infrastructure spending as a cyclical boost to offset the deleterious effects of Covid. Given that governments at all levels (national, state, and local) are serious about transitioning to EVs, they are going to have to facilitate the development of an EV ecosystem, including charging stations. This area could be on the cusp of a wave of capital.

Finally, COVID put a damper on the company’s foray into supplying airlines with materials handling equipment for baggage, etc. As one of the world’s largest polluters, airlines are eager to adopt greener solutions where possible. As a business with currently stressed balance sheets and depressed revenues, the improved cost associated with lithium-ion remain attractive, though the current purchase orders remain on hold as airlines wait for customers to return or help from the government.

This completely ignores artificial intelligence and some of the other light industrial and residential opportunities that have yet to be aggressively pursued.

Conversion from product sale to service

Probably the most impactful change for the company from a market perception perspective is its ability to transition a growing installed base (OEM and conversions) from transactional (buy battery -> install in forklift) to relational. Specifically, the company’s ability to leverage its telemetry and provide what is effectively power as a service to a large installed customer base.

The benefit for clients is easier oversight of its fleet, lower costs (both in terms of energy and human resources), and improved productivity through decreased downtime. For Flux, the benefit is stickier customer relationships, smoother revenue, and higher margins, as telemetry is more akin to a software sale, and has correspondingly high margins.

Valuation

Although the company has been around for over a decade, it did not pivot from its focus on being a supplier to automobile OEMs until 2013, and has spent most of that time developing the technology and infrastructure required to compete for large opportunities. While this has tested the patience of investors (as did a deeply discounted secondary offering in August 2020), the company seems to be at an inflection point where the market will begin to give it credit for what is likely to be continued rapid growth in its top line. Accordingly, we value the company using a multiple of revenue, with belief that profitability and cash flow will follow as the business scales.

Base Case

The closest proxy is probably Romeo Power Technology (Romeo), which is being brought public via a SPAC, RMG Acquisition Corp: (NYSE: RMG). Romeo focuses on batteries for trucks though, unlike Flux, it has its own proprietary battery manufacturing facility. Romeo’s equity value of $1.3 billion post-money is based on projected revenues of $765M in 2023, or 1.7x sales. At even half of its three-year sales growth rate of 165%, this would value Flux at over 50% above its current market cap.

Upside Scenario

We think the company’s progress from a revenue perspective has the potential to move in step changes and accelerate at a much more rapid rate. For a company of this size, all it takes is one or two large orders to accelerate growth exponentially. Currently, the company has a four-person sales team, predominantly focused on OEMs. It partners with Averest, Inc. to distribute to airports/airlines; it seems like this partnership model should be expanded to other verticals and/or the sales team should be expanded, given the product suite and the capacity at the current facility to accommodate up to $100m in revenue, which, if achieved, would put its market cap at roughly double.

In a blue-sky scenario, Flux gains a low-single digit share of the $11 billion materials handling lithium-ion battery sector plus parleys its relationship with Beam into a significant source of revenue from the buildout of EV charging stations globally. Moreover, although the largest materials handling companies currently use hydrogen almost exclusively, opportunities exist as the growth of companies like Amazon into new verticals introduces the potential for lithium-ion solutions to be a viable alternative in certain cases. Any of these events would put the stock order of magnitude above current levels, even if accounting for capital raises that may be required to support such dynamic growth. We would be optimistic that organic cash flow could make the company self-funding by that point, though our experience shows external capital is often required.

Downside Scenario

Flux has a smaller market cap than most companies we own, which presents challenges.

Although its recent equity issuance shored the balance sheet, the company’s finances could become stretched in the event of a global economic downturn, and historically it has paid relatively usurious rates for working capital financing and debt, with some of the latter potentially dilutive. Risk of material dilution remains an overhang, especially with the company’s filing on October 16, 2020 of a $50 million mixed shelf. We would not expect the shelf to be tapped except in the event of an accretive acquisition. The company also has warranty obligations associated with the sale of its batteries. It does have patent-protected intellectual property, though only a few patents, and its supply chain is heavily reliant on Chinese suppliers, exposing the company to political risk as well as potential capacity issues as production ramps.

What could unlock the value?

Formidable believes any of the following events could help the market begin to close the gap between FLUX’s current price and our estimates of fair value. Each event has a reasonable probability of coming to fruition:

- Strategic acquisition – This could go either direction. Flux seems interested in accumulating and acquiring interests in vendors, supply chains, competitors etc. Its CEO, Ron Dutt, is an experienced acquiror. This would indicate potential appetite for the company become a vertically integrated provider of small and large lithium batteries to its customers. Currently, Flux has a large OEM that is extremely pleased with its work. This is creating collateral momentum within the space and other large OEMs are beginning to come to the table. The addressable market in this respect can become very dynamic and Flux is in a position, after the recent capital raise, to step up and meet these opportunities. This is what we believe will become the Flux flex.

Conversely, Flux could itself be acquired by a legacy battery maker looking to complement a legacy battery business. This scenario transpired with Navistar, a private competitor. Terms were not disclosed, but after a few years of trying to develop its own technology, East Penn acquired Navistar, seemingly deciding it was easier to buy than build.3

- Structural improvements in market perception –In this era of factor-based and index investing, companies need a certain level of market cap and liquidity to hit the screens for most institutions. Flux has now checked the box in terms of:

- Market cap – near $100m as of 11/3/2020.

- Exchange listing – Uplisted to NASDAQ August 2020.

- Liquidity – average daily dollar volume of $3 million since its uplisting.

- Average volume – 485k shares

- Average price – $6.55

- Favorable legislation – The possibility of a “Green New Deal”—a widely reported Democratic initiative and talking point. Government programs aimed at reducing emissions and incentivizing the shift to EVs would also be a positive.

Conclusion—The Adoption Juggernaut

In the last 20 years we have seen multiple iterations of the same behavior within industries. The adoption of the Internet, the embracing electric vehicles and alternative power sources away from fossil fuels, the emergence of hand-held portable devices and information processing that with blistering speed and tremendous capacity. We cannot say with any certainty that the power source Flux provides to its customers will be adopted quickly, but if history is an analog, then the momentum we are currently seeing in orders could be breathtaking. We would be unsurprised by this phenomenon, having seen it multiple times before.

So, is Flux a niche provider? Maybe not. The applications for these types of battery and power types are only growing in size and impact. The broad spectrum of applications is undeterminable, because of its sheer size. Formidable believes that lithium is the oil of tomorrow and that the pick and shovel approach that Flux power is serving is likely to expand geometrically. One might think of themselves as being on the train and realizing that the train and the station are both moving at quantum speeds. The adoption of lithium battery solutions is an inevitability, in our minds, and a forgone conclusion.

Footnotes

1 – NASDAQ: FLUX

2 – Link to 13G Filing

3 – Accessed November 4, 2020 via url: http://www.energystoragejournal.com/east-penn-buys-lithium-battery-manufacturer-navitas-systems/

DISCLOSURES

General Firm

Formidable Asset Management, LLC (Formidable) is an investment adviser registered under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, Formidable cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of Formidable and may not actually come to pass. This information is current as of the date of this material and is subject to change at any time, based on market and other conditions. Any index performance cited or used throughout is intended to illustrate historical market trends and performance. Indexes are managed and do not incur investment management fees. An investor is unable to invest in an index. The performance shown may not reflect a Formidable portfolio.

Past performance is no guarantee of future results.

Reader should assume that future performance of any specific investment or investment strategy (including the investments and/or investment strategies discussed in these materials) made reference to directly or indirectly in these materials will be profitable or equal the corresponding indicated performance level(s). Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results.

Specific Securities

The mention of specific securities and sectors illustrates the application of our investment approach only and is not to be considered a recommendation by Formidable. The specific securities identified and described above do not represent all of the securities purchased and sold for the portfolio, and it should not be assumed that investment in these securities were or will be profitable. There is no assurance that the securities purchased remain in the portfolio or that securities sold have not been repurchased. Charts, diagrams and graphs, by themselves, cannot be used to make investment decisions. You may contact Formidable Asset Management, LLC for a full list of recommendations made during the preceding period one year

Not an Offer

These materials do not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or any other product or service by Formidable or any other third party regardless of whether such security, product or service is referenced here. Furthermore, nothing in these materials is intended to provide tax, legal, or investment advice and nothing in these materials should be construed as a recommendation to buy, sell, or hold any investment or security or to engage in any investment strategy or transaction. Formidable does not represent that the securities, products, or services discussed here are suitable for any particular investor. You are solely responsible for determining whether any investment, investment strategy, security or related transaction is appropriate for you based on your personal investment objectives, financial circumstances and risk tolerance. You should consult your business advisor, attorney, or tax and accounting advisor regarding your specific business, legal or tax situation.

The opinions expressed here are those of Will Brown and Adam Eagleston are not intended as investment advice. They are also subject to change with changing market conditions. Clients of Formidable may have positions in securities discussed in this article. This writing is for informational purposes only—Formidable and the authors expressly disclaim all liability in respect to actions taken based on any or all of the information from this writing.

READY TO TALK?